Financial Readiness

Why pulling cash off a credit card is one of the most expensive ways to borrow.

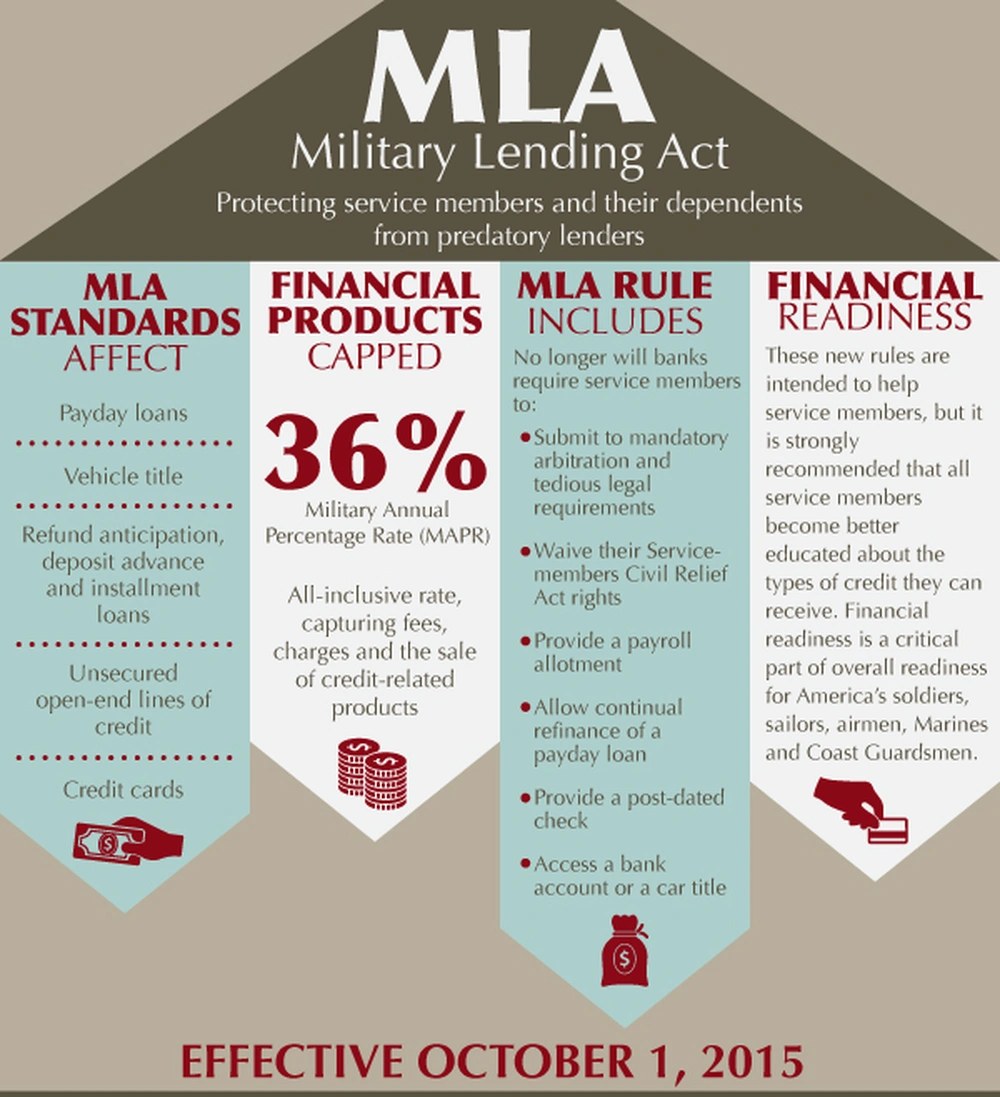

A graphic on Military Lending Act consumer protections for service members. Courtesy photo, DVIDS (public domain).

Upload your Leave & Earnings Statement and get a plain-English breakdown of every line.

Open LES Tool→A cash advance is cash you borrow against your credit card. It is one of the priciest ways to get money, because three charges hit at once: an upfront fee, often a minimum around $10; a higher interest rate, commonly 30 percent in card agreements; and no grace period, which is the window where you may owe no interest if you pay in full.

Here is the move that matters. Treat the cash advance option as a red flag, not a feature. Reach for cheaper cash first, and if you must use one, pay it down fast, because interest starts on day one.

A cash advance does not get charged like a normal purchase. Three costs land together, which is what makes it so expensive.

What it costs

$400 for one month: Carry a $400 cash advance for one month at 30 percent: about $10 in interest on top of a $20 fee, the equivalent of a 90 percent annual rate, even if you normally pay in full.

Treat the cash advance option as a red flag, not a feature.

Source: CFPB · figures illustrative

It is more than an ATM withdrawal. Convenience checks, the blank checks your card issuer mails you, are cash advances. So are most online gambling and sports bets, which major issuers largely treat as cash advances. Because some fees carry a flat minimum, a small $20 wager can draw the same $10 fee as a bigger pull.

A cash advance raises your balance, which raises your utilization. Utilization is the share of your limit you are using. A higher balance compared to your limit can weigh on your credit. The cleanest move is to keep the balance low and pay it down fast, since interest runs from day one.

Reach for cheaper cash before you tap the card. A small emergency fund covers most everyday surprises. A military aid society can offer an interest-free or low-cost loan for the military community. An on-base financial counselor can help you set up the cushion that keeps you off the cash advance button.

Some charges count as cash advances even when they do not feel like one. Here is what triggers the fee, and the cheaper moves to reach for first.

Counts as a cash advance

Reach for this instead

It raises your utilization too, which can weigh on your credit.

Source: CFPB · Military OneSource

You do not have to figure this out alone. Each branch has a military aid society, a nonprofit that offers interest-free and low-cost emergency loans for the military community. On-base financial counselors can help you build the cushion that keeps you off the cash advance button. You can find both through Military OneSource. If a card fee or bill looks wrong, the CFPB lets you file a complaint. All three are linked in Sources below.

Can I avoid interest by paying it back fast?

Not entirely. Interest starts at the transaction date with no grace period. Paying fast limits how much interest piles up.

Is the cash advance rate the same as my purchase rate?

Usually not. The cash advance rate tends to be higher, commonly 30 percent in card agreements.

Does using my card at a sportsbook count?

Often yes. Major issuers largely treat online gambling and legal wagers as cash advances, so the fee and the day-one interest can both apply.

Comments

Share your experience or ask a question. Comments are reviewed by our team before they appear.

Leave a comment