Financial Readiness

A plan that survives the 1st-and-15th cycle so your check lasts past the 20th.

U.S. military photo, DVIDS (public domain)

Upload your Leave & Earnings Statement and get a plain-English breakdown of every line.

Open LES Tool→A budget is not a punishment. It is a plan for every dollar before it lands, so your pay goes where you tell it instead of vanishing by the 20th.

Build it in this order: start from your take-home, give every dollar a job, and automate your savings so it is gone before you can spend it.

Work the steps in order. Start from your take-home, the only number that counts, and finish by paying yourself first.

Then pay yourself first:

Automate both the day you are paid, so saving never depends on willpower.

If you do nothing else: pay yourself first, and watch the calendar as closely as the dollar amount.

Source: DoD Office of Financial Readiness (FINRED), TSP.gov. Figures illustrative.

The number on the recruiter's slide is not the number that hits your account. Base pay is taxed. Your BAH and BAS allowances are not. Your take-home is its own number, and it is the only one your budget uses. Find it as net pay on your LES, then plan from there.

You get paid twice a month, on the 1st and the 15th. For junior service members, most money stress comes from timing, not from earning too little: rent hits on the 1st while the paycheck that covers it lands on the 15th. Call your billers, move due dates to line up with your paydays, and the same pay stretches further.

The habit that pays off most is to save before you can spend. The box above has the numbers. What makes them stick is automation: transfers that run on payday happen before you can spend the money, so the emergency fund builds and the TSP match lands without relying on willpower.

Your pay lands on a schedule, a big chunk of it is tax-free, and there is free retirement money waiting. Plan around all three and your paycheck stretches further than the number on the slide.

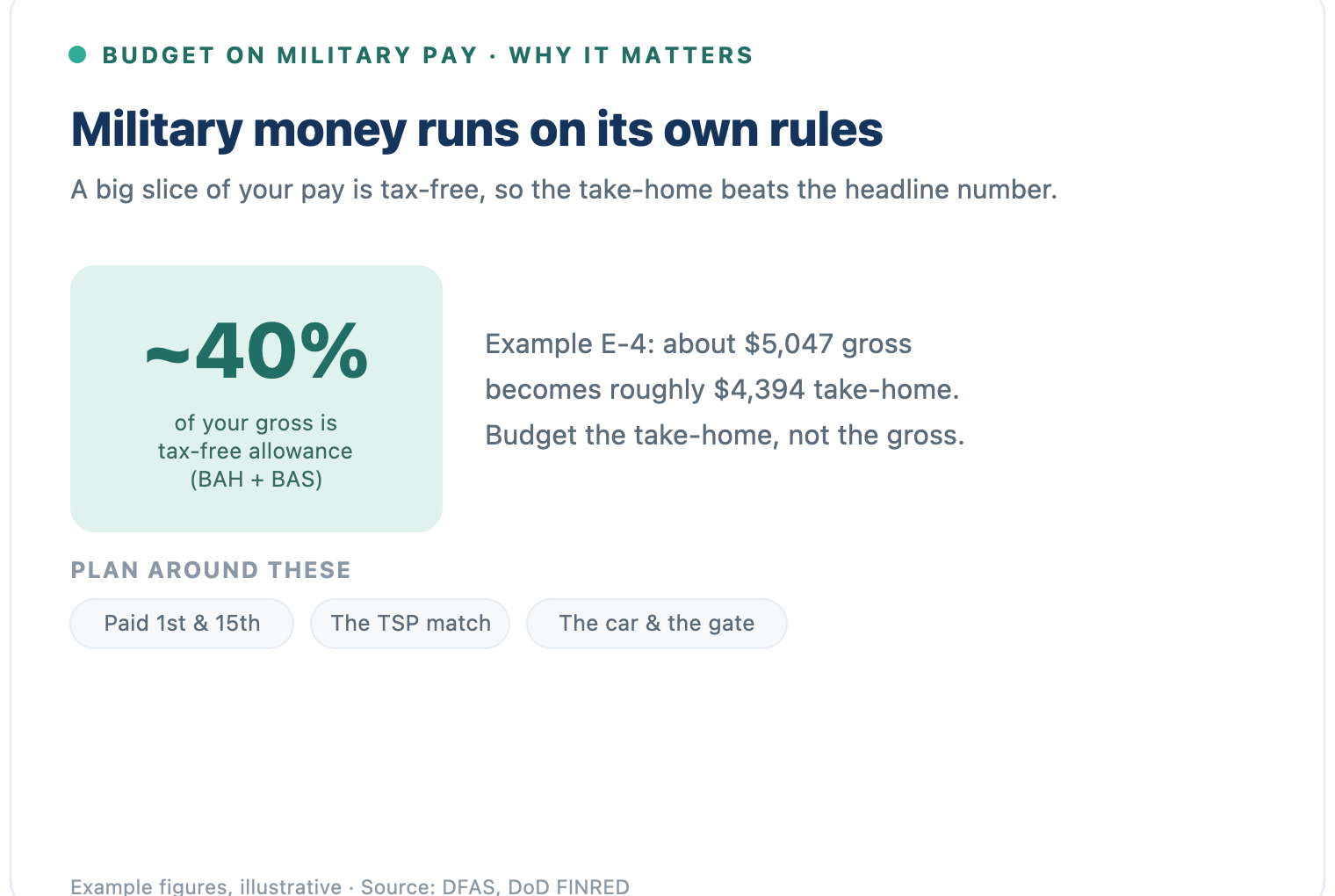

About 40% of your gross is tax-free allowance (BAH and BAS), money a civilian salary would be taxed on. Example E-4: about $5,047 gross becomes roughly $4,394 take-home. Budget the take-home, never the gross.

Plan around these:

Time your bills to your paydays, grab the full TSP match, and keep clear of the lenders at the gate.

Source: DFAS, IRS Pub 3, TSP.gov, CFPB. Figures illustrative.

The car. Service members pay more in interest and fees on auto loans than civilians, and most get talked into add-ons like extended warranties and GAP. Budget the real cost, insurance included, before you sign.

Lifestyle creep. Every raise is an invitation to spend more. Give the raise a job before it shows up in your account.

Predatory loans. Payday and title lenders sit outside the gate for a reason. A budget plus a starter fund is what keeps you from ever needing them.

Every active-duty, Guard, and reserve member, and their family, can get free one-on-one financial counseling through a Personal Financial Counselor. You will find counselors and free spending-plan tools through Military OneSource, the DoD Office of Financial Readiness, and the CFPB. All three are linked in Sources below.

Do my allowances count as income when I budget?

Yes. Money is money for budgeting. Just remember BAH and BAS are not taxed while base pay is, so plan from your LES net pay.

What is the first thing I should do with a raise or bonus?

Decide where it goes before it arrives, ideally toward your starter fund and TSP, so it does not melt into everyday spending.

Comments

Share your experience or ask a question. Comments are reviewed by our team before they appear.

Leave a comment